AML3D (AL3.AX)

Make shipbuilding great again.

Price: A$0.135

Fully diluted shares outstanding: 620.8m

Market cap: A$83.8m

Enterprise value: A$57.3m (excluding A$1.7m in lease liabilities)

EV/Sales (ttm): 9.5x

TLDR

Supplier of large-scale metal 3D-printers becoming embedded in the US Navy’s Maritime Industrial Base (MIB) supply chain.

Stock looks expensive at 9.5x ttm EV/sales, but the business is transitioning from early qualification work to full-rate production.

AML3D received a non-binding US Navy Letter of Intent (LOI) for up to 100 systems through 2030 (current installed base: ~13 systems), which could lead to a revenue base several times larger than today.

Excellent unit economics, with 60% gross margin on equipment sales and 75% on annual license and support fees. With a growing installed base, this can support 20% operating margins at scale.

$A26.5m in net cash (~30% of market cap), enough to fund growth investments.

Introduction

I’ve owned AML3D for over a year now. It’s a small position, because it’s speculative. But instead of just letting it sit in my portfolio, the stock has occupied way too much head space. I’m constantly torn between „you don’t own enough“ and „this thing trades at 10x EV/sales, you idiot“. So this write-up is my final attempt to get this thing out of my head and convince myself that it can be OK to pay a seemingly high EV/sales multiple.

Company description

AML3D manufactures large-scale wire-arc additive manufacturing (WAAM) systems, typically used to 3-D print very large components, with build volumes of up to 36 cubic metres. Its core product is the ARCEMY X. It uses off-the-shelf robotics and a welding torch to deposit molten metal from weld wire feedstock onto a substrate along a programmed path.

Although AML3D is headquartered in North Plympton, Australia, the commercial focus shifted to the US in 2023, when the company launched its US “Scale up” strategy. In late 2024, this led AML3D to open a production facility in Stow, Ohio to qualify for ITAR-controlled and “US-only” defence contracts. Capacity expansion is now underway to meet the Navy’s expected demand.

AML3D’s technology is patented in Australia, New Zealand, Japan, and Europe. The company has also applied for a patent in the US.

Why now?

The US Navy is clearly moving additive manufacturing (AM) from R&D and into production. In 2025, it installed 3D-printed parts on both an aircraft carrier and a Virginia-class submarine and began integrating AM parts into the supply chain. AML3D should be able to benefit from this shift because, in 2024, the Navy’s Science & Technology Board specifically recommended prioritizing WAAM - AML3D’s core competency - for large parts.

The funding to expand WAAM capacity is also in place. The One Big Beautiful Bill (OBBB) has a dedicated $450m line item to increase weld wire production capacity, grow AM part production and machining capacity needed to finish AM parts.

Weld wire is the key feedstock for WAAM, and the Navy’s Science & Technology Board has flagged the Navy’s dependence on German producers of nickel-aluminium-bronze (NAB) weld wire. The Navy aggressively expanding its own weld wire production (demand expected to increase by 1200% over next 5 years to nearly 5m pounds) speaks to the strategic importance of WAAM. There is also a $50m line item in the OBBB to expand additive manufacturing capacity for naval propellers, which are commonly manufactured using NAB. I think both of these line items can be linked to AML3D, because they’ve received multiple contracts for NAB testing/qualification from the Navy and, recently, their first contract for the production of five non-safety-critical NAB parts. It’s probably also no coincidence that AML3D has already demonstrated that they can manufacture NAB propeller blades specifically.

Granted, there are other companies with similar capabilities, but AML3D has done the groundwork over the past few years to be well positioned to benefit from the Navy’s AM/WAAM rollout.

Note: I’m not going into detail about two more line items in the OBBB that provide $700M in funding to advancing AM and could also benefit AML3D. The wording is too broad to link either of them directly to AML3D/WAAM.

Customer integration and market position

Over the past three years, AML3D has leveraged its know-how to manufacture prototypes and provide material characterization services for the US Navy. These were the first steps toward qualifying the ARCEMY system for production of selected components. Importantly, once an ARCEMY-based manufacturing process is qualified for a particular component, switching to a system from another manufacturer would likely require lengthy requalification. This creates meaningful switching costs, reinforced by the necessary operator training, process development (e.g. welding parameters, deposition rates, etc.) and process documentation. According to AML3D’s management, the company has not yet encountered direct competition for the ARCEMY system in the US. AML3D’s CEO mentioned in an interview that all contracts with the Navy were procured as a “sole-source award”.

AML3D’s most notable customer is Huntington Ingalls (HII), the largest shipbuilder in the US. HII ordered its first two custom-made ARCEMY X systems in October 2025 and placed a follow-on order for four additional systems in March 2026. Austal USA, another prime contractor, operates a total of three ARCEMY systems at the U.S. Navy Additive Manufacturing Center of Excellence (AM CoE). The AM CoE is an operational hub to develop, qualify and transfer AM processes into the MIB. Other smaller Navy suppliers that operate ARCEMY systems are Laser Welding Solutions, Fastech and Cogitic. Cogitic is quite interesting, because it is a supplier of critical components for the Navy’s nuclear-powered submarines.

Side note: Cogitic also has a very cool corporate slogan:

One competitor for contract manufacturing services is vertically-integrated Lincoln Electric (ticker: LECO), which leverages its own proprietary platform to sell finished WAAM parts. In September 2025, Lincoln Electric announced a US Navy-funded partnership with General Dynamics Electric Boat to produce submarine components. However, they do not offer complete WAAM systems. If Lincoln Electric were to start selling its own systems, especially to a prime contractor for the Navy, that would be a clear competitive warning sign.

GEFERTEC is another company worth monitoring closely. They introduced a new WAAM machine that is capable of printing large components, with build volumes of up to 8 cubic meters. One of GEFERTEC’s smaller systems is installed in the US Navy AM CoE (alongside three ARCEMY systems). Fastech, a supplier of parts for defense, aerospace, and energy applications, recently ordered an ARCEMY system, even though it was already operating two GEFERTEC systems. This suggests to me that ARCEMY offers technical capabilities that Fastec couldn’t obtain from its GEFERTEC systems.

As things stand, the Navy appears to be pursuing two different sourcing models: centralized parts production, as in the case of Lincoln Electric, and supplier-owned production capacity (often through SMEs) in the case of AML3D/GEFERTEC.

Growth potential

A remarkable coincidence occurred on July 4 2025, because on the same day the OBBB was signed, AML3D received a Letter of Intent (LOI) from the US Navy. The LOI clearly demonstrates that the company possesses a technology that is of strategic interest to the Navy. It includes the following key points:

Demand forecast: the US Navy will provide AML3D with regular demand forecasts so that the company can strategically scale up its manufacturing capabilities.

Manufacturing of parts: the US Navy wants to 4x the number of 3D-printed parts over the next five years.

System sales: the US Navy's demand forecast shows a need for up to 100 systems over the next five years and highlights AML3D's “pivotal role in achieving these targeted needs”.

Coincidentally, the ASX asked AML3D to clarify when it became aware of the letter. In that response, the company disclosed that it had held discussions with representatives of the Navy for several months and checked the signed letter to confirm the commercial discussions were accurately reflected.

The main pushback is that „this is just an LOI“, but there is clear evidence that the demand outlined in the LOI is converting into firm orders at an accelerated pace. In the twelve months following receipt of the LOI, AML3D has announced A$19.9m of new orders. This is roughly equal to the cumulative order value received during the previous 2.5 years.

AML3D’s management estimates a potential LOI-opportunity ranging from A$150m to A$200m. To put this into perspective, trailing twelve month revenue amounts to just A$6.0m. Even if AML3D cannot convert the full LOI-opportunity, it is still possible to generate a revenue base several times larger than today.

In summary, the combination of the LOI, available funding, policy backdrop (prioritising WAAM and “make shipbuilding great again”) and repeat orders from two Navy prime contractors, leads me to believe that AML3D will become a strategic WAAM equipment supplier for the Navy‘s MIB.

Unit economics and margin potential

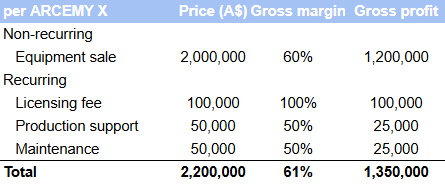

Although the company still offers contract manufacturing, management has shifted the strategic focus over the past three years to the sale of complete ARCEMY systems. In addition to the hardware, each system sale generates recurring revenue from licensing fees, production support and maintenance, at ~10% of the initial equipment sale, or A$0.2m per ARCEMY X system.

The unit economics of an ARCEMY X system indicate a differentiated niche product that does not primarily compete on price:

What the customer is paying for is most likely process IP, proprietary software and qualification know-how. 60% gross margin for a manufacturer of special machinery/equipment is unusually high, especially considering that the hardware is mostly off-the-shelve. Although the license fee is small relative to the equipment sale, a growing installed base can generate a very attractive recurring revenue stream.

Mature niche equipment manufacturers with gross margin profiles similar to AML3D’s can achieve operating margins of 20–30%, whereas high-technology equipment manufacturers with high R&D expenses tend to generate operating margins in the mid-teens. AML3D’s operating margin should fall somewhere in the middle of these two groups. I think 18–20% is realistic in the long term because a portion of AML3D’s R&D expenses are customer- and government-funded.

“Valuation”

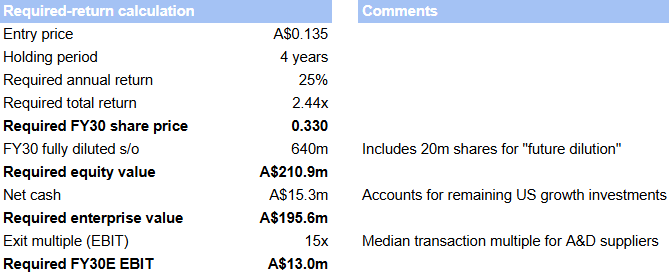

I won’t pretend that I can predict with a high degree of certainty how much revenue and what margins AML3D will generate in FY30 (roughly in line with the LOI timeline). The timing of orders and commissioning of systems plays too big a role for that. Instead, I’m trying to “reverse-engineer” what must be true in order for me to achieve an IRR of 25% (2.44x over four years):

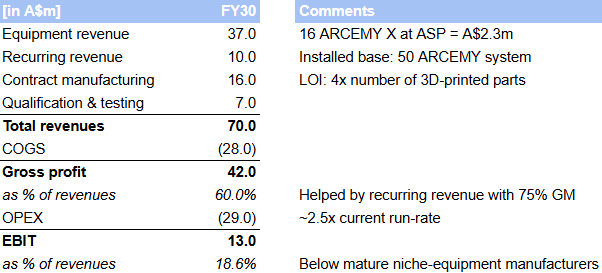

Using the FY30E EBIT of A$13.0m and an exit multiple of 15x EBIT, an illustrative P&L could look like this:

Again, this is not meant to be a forecast, but rather a sanity check on whether AML3D’s margin and growth potential are compatible with the investment thesis, that the ARCEMY system becomes a standard equipment within the Navy’s MIB.

None of the underlying assumptions strike me as completely unrealistic. I’ve already touched on why I believe that a 18-20% operating margin is achievable. And while a larger revenue share of contract manufacturing could weigh on gross margins, this may be offset by a growing installed base and the associated high-margin recurring revenues (licensing/support/maintenance).

Increasing revenue by nearly 12x the current revenue base definitely looks aggressive (crazy) and carries considerable execution risk. However, it does not depend on AML3D converting the full 100 ARCEMY-system opportunity and gives no credit to other growth opportunities, like a Boeing manufacturing license agreement, additional Tennessee Valley Authority (largest public utility in the US) purchase orders or UK demand signals (BAE qualification work and component order from undisclosed defence prime).

The combination of multibagger potential and high execution risk is why I’ve sized the position at only 3%.

Risks

The main risk is that I’ve misjudged AML3D‘s role within the MIB and it remains a sub-scale equipment supplier, with ARCEMY orders coming through only occasionally. I think the evidence laid out above argues against this, but I cannot rule out that, after putting far too much work into the stock, I’ve simply created a nice story to justify paying a way too high multiple.

I also cannot rule out further dilution, despite the company sitting on A$26.5m in net cash. A$11.2m remains earmarked for its US expansion (and A$5.0m conditional on sufficient demand). If project timelines slip and multi-system orders get delayed, AML3D could still need to raise more equity.

Finally, scaling revenues by >10x over a short period carries substantial execution risk, especially if customers demand customized systems rather than more standardized equipment, whhich could also weigh on margins.

I own shares in AML3D. This is not investment advice, just my personal, biased opinion. Always do your own due diligence.

Fascinating. Very interesting company. My only advice is better to pay up when they become operating income positive on a given quarter before going big. And you will the first to know. There are companies that seems to be pushing that goalpost… every year. Also tool maker are often a less interesting business than the one using it (safran aeroedge hintington)

Well well well look who has risen from the dead.